All Categories

Featured

Table of Contents

The are entire life insurance and universal life insurance policy. The money value is not added to the death advantage.

After one decade, the cash worth has actually grown to around $150,000. He gets a tax-free car loan of $50,000 to begin a company with his sibling. The plan financing rates of interest is 6%. He pays back the funding over the next 5 years. Going this path, the rate of interest he pays goes back into his plan's cash money worth as opposed to a monetary organization.

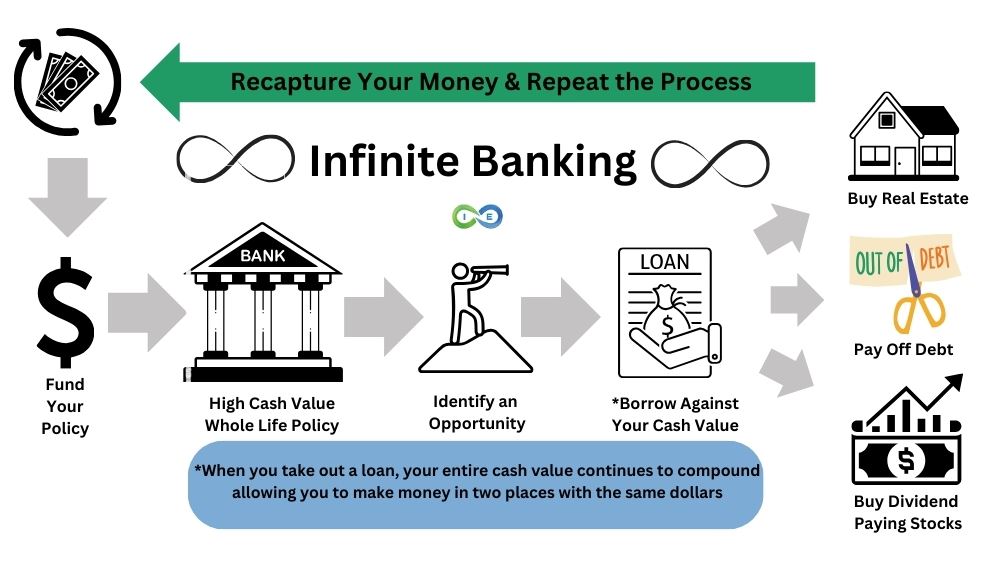

Imagine never having to worry regarding financial institution lendings or high rate of interest prices once again. That's the power of infinite banking life insurance coverage.

There's no collection car loan term, and you have the liberty to pick the repayment schedule, which can be as leisurely as repaying the loan at the time of death. This versatility reaches the servicing of the fundings, where you can choose interest-only settlements, maintaining the lending balance flat and convenient.

Holding cash in an IUL taken care of account being attributed interest can typically be much better than holding the cash money on deposit at a bank.: You've constantly fantasized of opening your own pastry shop. You can borrow from your IUL policy to cover the first expenses of leasing a space, purchasing devices, and working with team.

Infinite Banking Concept Book

Individual fundings can be obtained from traditional banks and cooperative credit union. Right here are some key factors to take into consideration. Credit report cards can supply a versatile way to borrow money for extremely temporary durations. Nevertheless, obtaining money on a charge card is generally very pricey with interest rate of passion (APR) typically getting to 20% to 30% or more a year.

The tax obligation therapy of policy car loans can differ significantly relying on your nation of residence and the certain terms of your IUL plan. In some regions, such as The United States and Canada, the United Arab Emirates, and Saudi Arabia, plan finances are generally tax-free, providing a significant benefit. Nevertheless, in various other jurisdictions, there may be tax effects to think about, such as possible taxes on the lending.

Term life insurance only offers a fatality benefit, without any type of money worth build-up. This suggests there's no money worth to borrow against.

Own Your Bank

When you first hear concerning the Infinite Banking Principle (IBC), your initial reaction may be: This appears too good to be true. Perhaps you're doubtful and assume Infinite Banking is a scam or scheme - cash flow banking with life insurance. We intend to establish the document directly! The trouble with the Infinite Banking Principle is not the idea but those persons offering an adverse critique of Infinite Banking as an idea.

So as IBC Authorized Practitioners via the Nelson Nash Institute, we believed we would certainly answer some of the leading questions individuals search for online when finding out and recognizing every little thing to do with the Infinite Banking Principle. So, what is Infinite Financial? Infinite Financial was produced by Nelson Nash in 2000 and completely clarified with the publication of his publication Becoming Your Own Lender: Open the Infinite Financial Concept.

Unlimited Banking Solutions

You believe you are coming out monetarily in advance due to the fact that you pay no interest, however you are not. When you save money for something, it normally suggests giving up something else and reducing back on your way of life in various other areas. You can duplicate this procedure, however you are merely "shrinking your way to wide range." Are you pleased living with such a reductionist or scarcity way of thinking? With saving and paying cash money, you may not pay interest, but you are utilizing your money once; when you spend it, it's gone for life, and you provide up on the opportunity to make life time compound interest on that particular money.

Billionaires such as Walt Disney, the Rockefeller household and Jim Pattison have actually leveraged the buildings of entire life insurance policy that goes back 174 years. Even financial institutions use whole life insurance policy for the exact same purposes. It is called Bank-Owned-Life-Insurance (BOLI). The Canada Revenue Firm (CRA) even identifies the worth of taking part entire life insurance coverage as an unique property course used to produce long-term equity securely and predictably and offer tax advantages outside the extent of typical investments.

Nelson Nash Life Insurance

It allows you to create riches by fulfilling the financial function in your very own life and the capacity to self-finance significant way of living acquisitions and expenditures without interrupting the substance interest. One of the most convenient ways to think concerning an IBC-type getting involved entire life insurance plan is it approaches paying a mortgage on a home.

In time, this would certainly produce a "continuous compounding" impact. You obtain the image! When you obtain from your taking part entire life insurance policy policy, the cash money value remains to grow continuous as if you never obtained from it in the initial area. This is due to the fact that you are using the money value and fatality benefit as security for a funding from the life insurance coverage company or as collateral from a third-party lender (called collateral borrowing).

That's why it's critical to deal with a Licensed Life Insurance Broker authorized in Infinite Financial who frameworks your participating entire life insurance coverage policy correctly so you can prevent negative tax implications. Infinite Banking as a monetary approach is not for everyone. Here are several of the pros and cons of Infinite Financial you need to seriously take into consideration in making a decision whether to progress.

Our preferred insurance policy service provider, Equitable Life of Canada, a shared life insurance policy company, specializes in participating whole life insurance policy plans details to Infinite Banking. In a common life insurance business, insurance holders are thought about firm co-owners and get a share of the divisible excess generated yearly through rewards. We have a variety of providers to select from, such as Canada Life, Manulife and Sunlight Lifedepending on the requirements of our customers.

Please additionally download our 5 Top Questions to Ask A Boundless Financial Representative Before You Employ Them. For additional information concerning Infinite Banking go to: Please note: The material offered in this e-newsletter is for informative and/or educational functions just. The information, opinions and/or views revealed in this e-newsletter are those of the authors and not necessarily those of the supplier.

How To Create Your Own Banking System

The idea of Infinite Banking was produced by Nelson Nash in the 1980s. Nash was a finance expert and fan of the Austrian institution of business economics, which promotes that the worth of products aren't clearly the result of conventional financial structures like supply and need. Rather, individuals value cash and products differently based on their financial status and demands.

One of the challenges of traditional financial, according to Nash, was high-interest rates on loans. A lot of people, himself consisted of, obtained right into monetary problem because of dependence on financial organizations. Long as banks established the passion prices and financing terms, people really did not have control over their very own wide range. Becoming your very own lender, Nash determined, would certainly put you in control over your economic future.

Infinite Banking needs you to have your monetary future. For ambitious individuals, it can be the best financial device ever before. Right here are the benefits of Infinite Banking: Arguably the single most advantageous facet of Infinite Banking is that it boosts your cash money circulation.

Dividend-paying whole life insurance policy is really reduced danger and provides you, the insurance holder, a good deal of control. The control that Infinite Financial offers can best be organized into 2 categories: tax obligation benefits and property defenses. One of the factors whole life insurance policy is excellent for Infinite Financial is just how it's taxed.

Entire life insurance policies are non-correlated properties. This is why they function so well as the financial structure of Infinite Financial. No matter what takes place in the marketplace (supply, property, or otherwise), your insurance coverage keeps its well worth. Way too many people are missing out on this important volatility barrier that assists secure and expand riches, instead dividing their money right into 2 buckets: checking account and investments.

Whole life insurance is that 3rd container. Not just is the rate of return on your entire life insurance policy guaranteed, your death advantage and premiums are also ensured.

Royal Bank Infinite Avion

Infinite Financial appeals to those seeking greater monetary control. Tax obligation effectiveness: The cash money worth grows tax-deferred, and policy financings are tax-free, making it a tax-efficient tool for developing wealth.

Property security: In several states, the money worth of life insurance policy is shielded from creditors, adding an additional layer of monetary safety. While Infinite Banking has its advantages, it isn't a one-size-fits-all option, and it features significant disadvantages. Here's why it might not be the most effective approach: Infinite Financial typically requires complex policy structuring, which can perplex policyholders.

{kind=link}

Latest Posts

How To Start Your Own Offshore Bank

Infinite Banking Vs Bank On Yourself

My Wallet Be Your Own Bank